The Seminar Summaries special report from the 22nd INTOSAI WGEA Assembly, held 22-24 January 2024, is now available on our website. The special report is based on the first day of the Assembly, which …

The INTOSAI WGEA surveys which overview the global public sector environmental audit practices have been conducted among the INTOSAI members in every three years since early 1990s, each culminating wi…

The INTOSAI WGEA Secretariat published a blog post in March on the recent expansion of the WGEA with three new members in 2023. In relation to this, SAI Vietnam and SAI Nepal provided short commentari…

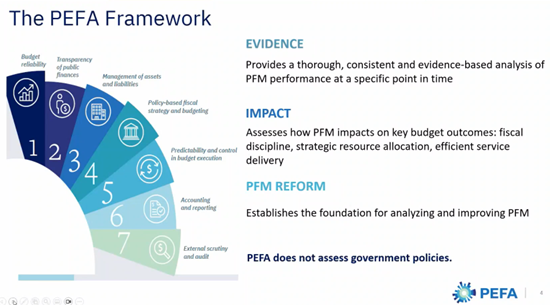

The webinar “PEFA and PEFA Climate: useful aspects for SAIs?”, held 14 March, is now available on the INTOSAI WGEA Youtube channel. The webinar discusses the Public Expenditure and Financial Accountab…

The 22nd INTOSAI WGEA Assembly Expert Interview videos are now available on the INTOSAI WGEA Youtube channel. The videos feature interviews on themes discussed at the Assembly such as environmental ch…

INTOSAI WGEA Secretariat will organize a Webinar on PEFA and PEFA Climate: useful aspects for SAIs?. The event will take place on Teams on Thursday 14 March at 12:00-13:00 UTC (8:00-9:00 AM Washington…

The INTOSAI Working Group on Environmental Auditing (WGEA) aims to increase the expertise in environmental auditing and to enhance environmental governance with high-quality contribution and visibility by both members of the Working Group and non–member SAIs. Currently the INTOSAI WGEA consists of 86 member countries.